Related Topics

What does retirement look like? For some people, it’s leisurely mornings, golf outings, and bucket-list vacations. But for older adults without enough retirement savings, the picture isn't quite as rosy. A recent survey by Clever found that 54% of older adults regret they didn't better manage their money before retiring. Similarly, 54% of retirees say they exited the workforce too soon.1

Importantly, not all of them retired by choice. When the pandemic sent the economy into recession, America's Great Retirement followed. Spurred by job loss, caregiving needs, burnout, medical issues, and fear of exposure to COVID-19, many workers retired sooner than planned. These early retirements were in stark contrast to what happened in prior economic downturns, when older adults delayed retirement to replenish their depleted savings.

Regardless of their reasons for retiring early, many older Americans now face economic uncertainty during what is supposed to be an enjoyable time of life.

Consider these eye-opening retirement statistics:

- Retirees only have a median of $142,500 in savings (four times less than the $572,000 experts recommend for starting retirement).1

- An alarming 25% of older adults who’ve officially left the workforce have nothing in savings at all.1

- Social Security is the major source of income for most Americans age 65 and older. However, the average monthly benefit of $1,782 in 2023 only replaces about 37% of past earnings for retirees who worked most of their adult lives.2,3

- During retirement, older adults outspend their annual income by more than $4,000 on average.4

The bottom line? Most older adults don’t have enough money put aside for retirement—and many face a real risk of outliving their savings. The shortfall each month requires many people to depend on savings accounts or investments to fill the gaps. A large portion of seniors also go into debt just to keep up with day-to-day living costs. In fact, Clever found that 2 of 3 retirees carries non-mortgage debt into their retirement years.

What can older adults do to lessen financial stress during retirement?

Adults facing financial instability in retirement need to leverage any money-saving tips they can. One important way to do this is through benefit programs that help low-income older adults pay for healthcare, prescriptions, food, housing, and more. Here are some programs to consider:

- Medicare Help: Are you having trouble affording your healthcare expenses? You may qualify for Medicare Savings Programs (MSPs), which were created for Medicare recipients with limited incomes who don't qualify for full Medicaid. These programs help older adults cover both Medicare premiums and out-of-pocket costs (e.g., deductibles). Four Medicare Savings Programs are available, each with its own income and resource criteria. If you're a Medicare beneficiary with limited income and assets, you may qualify for Medicare Extra Help. This program offers additional financial assistance with prescription drug costs.

- Energy Assistance: If you’re worried about heating your home in the chilly winter—or keeping it cool and comfortable in the summer, you may be able to get a helping hand. The federally funded Low-Income Home Energy Assistance Program (LIHEAP) provides grants to states, territories, the District of Columbia, and tribes to help eligible older adults pay their home heating and cooling costs. Every state has unique eligibility requirements and application processes. Another option for energy assistance is the Weatherization Assistance Program (WAP). This initiative helps eligible older adults lower their energy bills by making their homes more energy efficient—even if they rent or live in a multi-family complex.

- Wireless or Home Phone Bill Assistance: Your phone helps you stay connected to your family, friends, and community—but those monthly bills can really add up! Through the Lifeline phone discount program, older adults can receive monthly discounts on basic wireless or home telephone service. These savings may be in the form of free wireless minutes or a lower monthly phone bill. You may qualify for this program if you have limited income or if you're currently enrolled in programs like Medicaid or Supplemental Security Income (SSI).

- Housing Assistance: Retirees who haven't yet paid off their mortgage—or who face high and increasing rents—often face challenges staying in their home as they age. There are a host of programs available from the U.S. Department of Housing and Urban Development (HUD) to help eligible older adults manage their housing needs. The type of assistance provided varies, but you may be able to get help remaining in your current home or finding an apartment or retirement community. HUD also sponsors counseling agencies to advise older adults on issues such as foreclosures, evictions, and credit issues.

- Food Assistance: Do you feel like you’re able to purchase less and less on the same grocery budget each week? You’re not alone. With rising grocery prices, retirees on a fixed income are really feeling the squeeze. Fortunately, there are several food assistance programs that can offer relief for eligible households that are struggling to afford food. The most common is the Supplemental Nutrition Assistance Program, or SNAP (formerly known as food stamps). SNAP benefits are pre-loaded onto an Electronic Benefits Transfer (EBT) card, which can be used to buy eligible food in most retail stores that sell food (e.g., Walmart) as well as farmers markets. Wondering if SNAP is even worth applying for? You should know the average monthly benefit for a one-person senior household is $188.5

- Part-time (or full-time) jobs: A growing number of older adults are either returning to the workforce or seeking employment for the first time. There are several paths to employment for older adults. These include online job boards, newspaper ads, job fairs, and networking. NCOA recently launched its new employment tool, Job Skills CheckUp, to help older adults get tips on how to succeed as a mature worker. All you have to do is tell us about your goals, describe your current employment situation, and the Job Skills CheckUp will create a personalized plan to help you find job openings, build a professional network, prepare for job interviews, and more.

See if you qualify for any of these programs—all with NCOA's new and improved digital tool

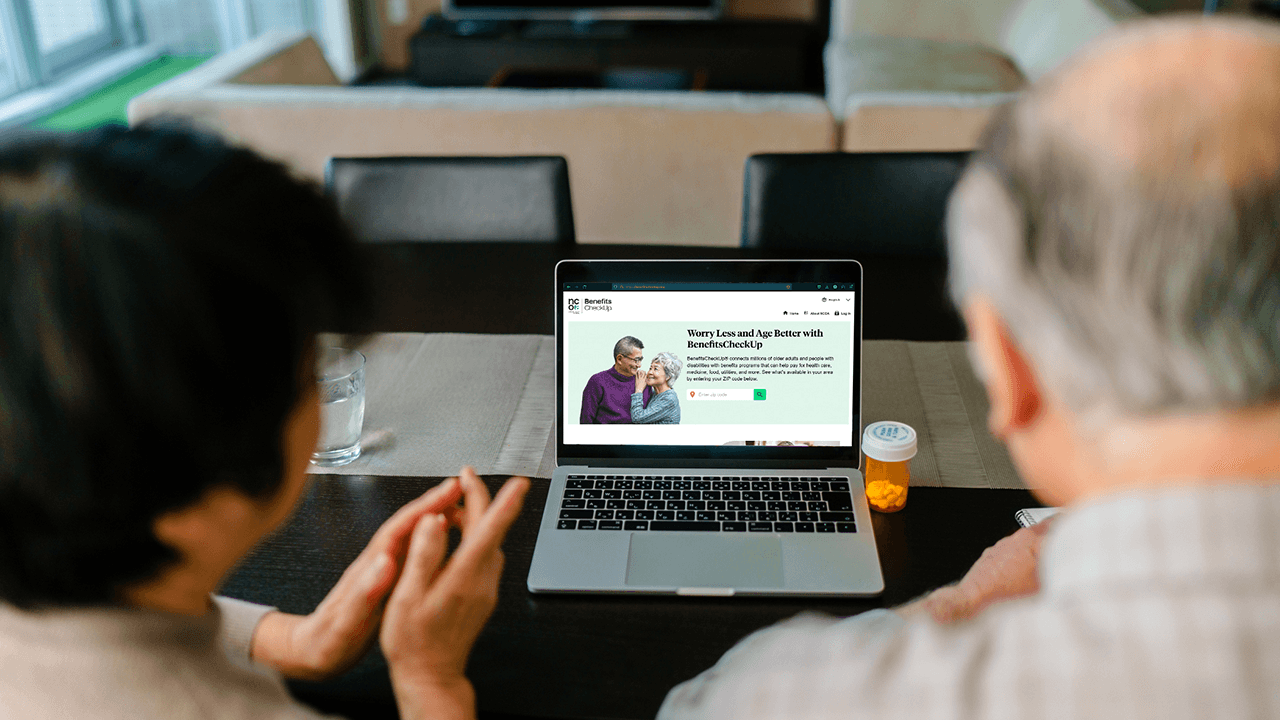

Navigating different benefit programs and their websites can be an overwhelming task. That's why NCOA created BenefitsCheckUp—a free, confidential, and easy-to-use tool that can help you uncover money-saving benefits that meet your needs.

These benefits can help you stretch your retirement dollars further and worry less. Just ask Ms. B., aged 63. Ms. B. lost her full-time job due to COVID-19 downsizing. When she went to talk to a benefits counselor at a local Benefits Enrollment Center she was desperate for help. They found out she qualified for $196 in SNAP benefits as well as $350 in LIHEAP utility assistance.

Because of this assistance, I don't have to go back to the part-time job I had," she told her benefits counselor. "These benefits have really helped me during these trying times."

Use BenefitsCheckUp for yourself or an older adult you know who needs help. Browsing for benefits takes just a few minutes, and there's no registration required.

Sources

1. State of Retirement Finances: 2024 Edition, Clever. Found on the internet at https://listwithclever.com/research/retirement-statistics-2024/

2. Social Security Basic Facts, Social Security Administration (2024). Found on the internet at https://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf

3. Policy Basics: Top Ten Facts About Social Security, Center on Budget and Policy Priorities (April 17, 2023). Found on the internet at https://www.cbpp.org/research/policy-basics-top-ten-facts-about-social-security

4. Annual Expenditures by Occupation, U.S. Bureau of Labor Statistics. Found on the internet at https://www.bls.gov/cex/tables/calendar-year/mean-item-share-average-standard-error/reference-person-occupation-2020.pdf

5. USDA. Characteristics of Supplemental Nutrition Assistance Program Households: Fiscal Year 2023. April 2025. Found on the internet at https://fns-prod.azureedge.us/sites/default/files/resource-files/snap-FY23-Characteristics-Report.pdf

Get Help Paying for Food, Medicine, and More

Millions of older adults miss out on money-saving benefits simply because they don't apply. Start today by answering a few questions to see if you qualify, and learn how to get help to apply