Related Topics

Nearly $54 billion. That’s the amount of unpaid medical bills older Americans were carrying in 2020—an increase of 20% from the year before. Another eye-opening fact? Among the nearly four million older adults with medical debt, nearly all of them reported having health insurance.1

Medical debt among seniors is a widespread problem. But before diving into the topic, it’s important to first understand what it means.

What is medical debt?

Medical debt refers to any outstanding (not paid by the due date) bills for health care services you received from a doctor, nurse, clinic, or hospital. While anyone can have medical debt, those more likely to be affected include older adults of color and older adults with low income.2

Shouldn’t health insurance prevent medical debt?

Even if you have Medicare or an employer-sponsored health plan, you still may be responsible for out-of-pocket costs like copayments, coinsurance, deductibles, and out-of-network surcharges. These costs can add up fast, especially if you have a chronic condition, serious illness, or disability. A single unexpected crisis—such as a car accident or bad fall—can plunge a person into debt quickly. In fact, most medical debt is due to bills from a one-time or short-term health care expense.

As if high out-of-pocket expenses weren’t bad enough, billing errors make older adults even more vulnerable to medical debt. Older people are more likely to have greater chronic health needs, which translates into a more complex billing process. This often leads to mistakes, such as the wrong parties being billed or providers seeking inappropriate reimbursement. Once an insurer rejects a claim, providers often continue to pursue patients for payment instead of fixing the error and resubmitting the claim. If patients don’t recognize their bill is inaccurate, unchecked errors can result in a snowball of medical debt that soon becomes unmanageable.

What are the dangers of medical debt?

Medical debt poses a major barrier to older Americans' economic and overall well-being. Some consequences of this type of debt include:

- Cutting spending on other necessities: Among older populations, 19% of those with unpaid medical bills find it very difficult to meet their monthly expenses, compared to 3.2% of those without medical debt.2 People who are trying to pay off medical debt are often forced to cut down on spending in other areas, such as food, medicine, and utilities. They may also postpone needed health care visits.

- Denial of future health care: A 2022 survey by Kaiser Family Foundation found that 15% of adults with medical debt were denied care due to unpaid bills.3

- Negative impact on credit score: If they go unpaid for a certain length of time, your medical bills can wind up in debt collection. Once that happens, you may be subject to unpleasant calls from debt collectors demanding prompt payment. If the debt remains unpaid, it can appear on your credit report and lower your credit score. This may impact your ability to take out a loan, secure housing, or even get a job.

While medical debt is considered consumer debt, it functions slightly differently than other kinds of debt. Most health care providers won't send an account to collections unless a bill is at least 60 days past due. Also, an unpaid medical bill won't hit your credit report until 180 days or more have passed since it became due. Lastly, the three credit bureaus (Equifax, Experian, and TransUnion) have recently taken steps to remove paid medical debt, debt less than a year old, and all medical collections under $500 from consumer credit reports.

Recent research by the Urban Institute showed that debt can have a harmful impact on older adults' physical health as well. Those who carry debt are more likely to develop conditions like depression, hypertension, and even cancer. 4

I am a senior with medical debt. What should I do?

If you’re having trouble paying your medical bills on time, don’t ignore them. Instead, explore these options:

- Review your bill(s) for errors: If you don't have one, ask for an itemized bill from your health care provider including all charges and associated codes. Scan it carefully for errors (such as a duplicate charge or service you did not receive). You should also compare the bill to any explanation of benefits (EOB) sent by your insurance company. If you have Original Medicare, you'll want to check your Medicare Summary Notice (MSN). That way, you can make sure everything that should be covered by your plan shows as covered on the bill.

- Try to negotiate down the total amount you owe: If you've determined your bill is accurate, call your provider to see if you qualify for a low- or no-interest payment plan. Some may accept a lower total amount in exchange for making a large deposit and paying the rest off over a period of time.

- Ask about financial assistance ("charity care"): Under the Affordable Care Act (ACA), nonprofit hospitals must provide free or discounted health care to those struggling to pay their medical bills. If it's an unpaid hospital bill you're facing, ask for a copy of their Financial Assistance Policy (FAP) and fill out an application. You can still apply for financial assistance if your bill is in collections. Also, even if the hospital where you received care is a private organization, they may still have a FAP—so be sure to inquire. There are also other hardship and financial assistance programs that help cover medical expenses for patients with limited means. These may be state-run or sponsored by providers, religious groups, and nonprofit organizations such as the Patient Access Network Foundation. Ask your health care provider or local area agency on aging (AAA) if they have recommendations for programs that may be able to help you.

- Hire a medical bill advocate: If you're buried under medical debt, a medical bill advocate will review your bills for accuracy and negotiate on your behalf. Although it costs money to hire a professional, it may be worth it if the money you owe is substantial. Visit the Alliance of Claims Assistance Professionals to find advocates near you.

- Consider a low-interest loan: If you have otherwise good credit and a healthy income, you may qualify for a low-rate personal loan. Another option may be a credit card with a 0% introductory interest rate. This will give you extra time to pay off your debt without accruing more interest or entering debt collection—but only do it if you know you can pay off the debt before the promotional period ends. Getting a loan or credit card should only be an option if you’ve exhausted all other avenues of repayment.

If you're unable to address your medical debt through any of the channels mentioned above, you may want to think about credit counseling. A debt counselor certified by the National Foundation for Credit Counseling (NFCC) can help you understand your choices and make a plan to regain control of your finances. Search for NFCC-certified counselors.

Medicare expert Brandy Bauer, former Director of the MIPPA Resource Center, says older adults should also look into federal and state programs for Medicare beneficiaries with limited means. While the programs below won’t cover existing debt, they can help prevent health care expenses from mounting:

“If you have low income and meet other requirements, these programs can help pay for costs above and beyond what Medicare covers and make a dramatic difference in your out-of-pocket spending,” Bauer explains. “It’s well worth taking the time to find out if you qualify.”

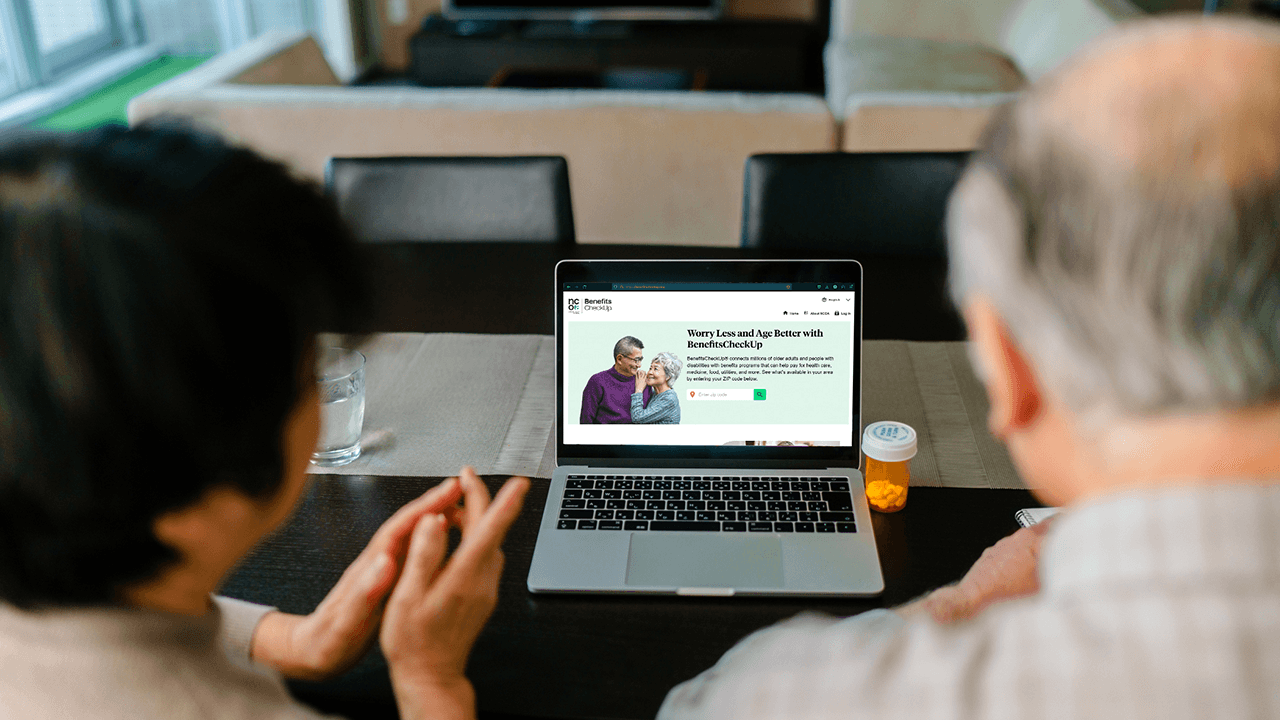

To learn about these and other programs that can help you save money, visit BenefitsCheckUp.org. You can also explore resources on managing debt in our Debt for Older Adults resource library.

Sources

1. Consumer Financial Protection Bureau. Medical Billing and Collections Among Older Americans. May 30, 2023. Found on the internet at https://www.consumerfinance.gov/data-research/research-reports/issue-spotlight-medical-billing-and-collections-among-older-americans/full-report/

2. Consumer Financial Protection Bureau. 2023. Estimates using data from the 2018 FINRA Foundation National Financial Capability Study. Presented at Age + Action Virtual, June 21, 2023.

3. Lunna Lopes, et. al. Health Care Debt In The U.S.: The Broad Consequences Of Medical And Dental Bills. Kaiser Family Foundation. June 2022. Found on the internet at https://www.kff.org/health-costs/report/kff-health-care-debt-survey/

4. Stipica Mudrazija and Barbara A. Butrica. Center for Retirement Research at Boston College. How Does Debt Shape Health Outcomes for Older Americans? November 2021. Found on the internet at https://crr.bc.edu/wp-content/uploads/2021/11/wp_2021-17.pdf

Get Help Paying for Food, Medicine, and More

Millions of older adults miss out on money-saving benefits simply because they don't apply. Start today by answering a few questions to see if you qualify, and learn how to get help to apply