When it comes to Medicare enrollment, there are certain rules to keep in mind. Not following these rules can come with risks. One risk you should know about is Medicare's late enrollment penalties.

What are the Medicare penalties for late enrollment?

Late enrollment penalties are additional amounts you may have to pay permanently if you dont' sign up for certain parts of Medicare when you're first eligible (and you don't qualify for a Special Enrollment Period).

Below is an overview of how penalties apply to each part of Medicare. We'll also explain how to avoid these fees and ensure your Medicare experience is as seamless and pain-free as possible.

| Medicare Part A Penalty | A 10% increase in your monthly premium. You'll have to pay the Part A penalty for twice the number of years you delayed enrolling (Note: Most people do not pay a Part A premium). |

|---|---|

| Medicare Part B Penalty | Adds 10% to your monthly premium ($202.90 in 2026 for most people) for each full 12-month period you waited to sign up. You will pay the Part B penalty for as long as you have this coverage. |

| Medicare Part D Penalty | 1% of the national base beneficiary premium ($38.99 in 2026) for each month you delayed. It's added to your monthly Part D premium for as long as you have this coverage. |

Medicare Part A penalty

Most people are entitled to Part A for free since they paid the Medicare tax while still working. But if you have to pay a premium for Medicare Part A and you don't sign up when you're first eligible, you may face a late enrollment penalty. This penalty is a 10% increase in your monthly premium, and you'll have to pay it for twice the number of years you delayed enrolling. In 2026, those with premium Part A will pay either the full premium or a prorated amount (between $311 and $565 monthly).

Medicare Part B penalty

If you delay enrolling in Medicare Part B and don't have other qualifying coverage, you may face a late enrollment penalty. This penalty adds 10% to your monthly premium ($202.90 in 2026) for each full 12-month period you waited to sign up. You'll pay it for as long as you have Part B—potentially for life. If you are eligible for a Special Enrollment Period, this penalty can be avoided.

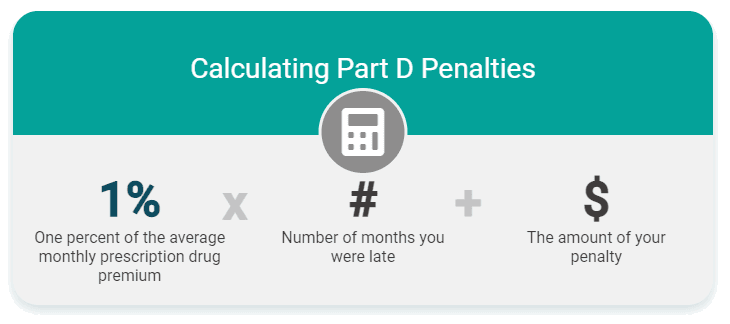

Medicare Part D penalty

If you go 63 days or more without Medicare drug coverage or other creditable prescription coverage after you're first eligible, you'll face a Part D late enrollment penalty. The penalty is 1% of the national base beneficiary premium ($38.99 in 2026) for each month you delayed. That figure is rounded to the nearest $.10 and added to your monthly Part D premium for as long as you have Part D. In 2026, the average basic premium for a stand-alone Medicare Part D plan is estimated to be about $34.50 per month.

If you are eligible for the Part D Low Income Subsidy (Extra Help) or a Special Enrollment Period due to having credible drug coverage, late enrollment penalties are not applied.

Creditable coverage is health or drug coverage that meets Medicare's standards, meaning it's expected to pay at least as much as Medicare would. Examples of creditable coverage include:

- Coverage through your job or your spouse’s job

- Retiree coverage

- Coverage through the Veterans Administration

Here's an example of the Part D late enrollment penalty in action:

Gil waited 20 months after becoming eligible to enroll in Medicare Part D and didn't have any creditable prescription drug coverage during that time.

Because of this, Gil now faces a late enrollment penalty. The penalty is 1% of the national base beneficiary premium for each month he delayed—so that's 20 x 1% = 20%. In 2026, the national base beneficiary premium is $38.99, so 20% of that is $7.80. This amount is rounded to the nearest $.10. That means $7.40 gets added to Gil's monthly Part D premium and he'll continue to pay it for as long as he has Part D coverage.

“Planning ahead can help you enroll in Medicare with confidence and avoid penalties that could plague you for years,” said Ryan Ramsey, NCOA Associate Director of Health Coverage and Benefits. “Since the rules around when to enroll can vary based on your personal circumstances, it’s important to review your options carefully and get expert guidance if you need it.”