When you turn 65, you’re eligible to enroll in Medicare. But timing matters. Medicare enrollment periods are specific timeframes during which you can sign up for or make changes to your Medicare coverage. This includes the Initial Enrollment Period (IEP)—the seven-month period that spans the three months before you turn 65, your birthday month, and the three months after.

The Annual Open Enrollment Period (OEP) is another one. This period runs from Oct. 15 to Dec. 7 each year and allows you to make changes to your Medicare Advantage (Part C) plan or Part D (prescription drug) plan.

Can you change Medicare coverage at any time?

Is it possible to make changes to your Medicare coverage outside of the usual windows? The answer is yes—if you meet the conditions for a Special Enrollment Period (SEP).

"Medicare Special Enrollment Periods give you flexibility when life or work circumstances delay your enrollment," said Ryan Ramsey, NCOA Associate Director of Health Coverage and Benefits. "When used correctly, an SEP allows you to sign up for Medicare without late penalties or gaps in coverage."

Below, we explore Medicare Special Enrollment Periods, including what they are, when you might qualify, and how you can take advantage of these unique opportunities to adjust your health care coverage.

What are Special Enrollment Periods?

These are specific enrollment periods that apply when you’re eligible for delayed enrollment in Medicare Parts A, B, C, and D. SEPs are only available if you’re affected by a qualifying life event, such as losing your existing health coverage or moving to another state. Medicare SEPs give you a chance to enroll in a plan without penalty.

Special Enrollment Period for Parts A and B

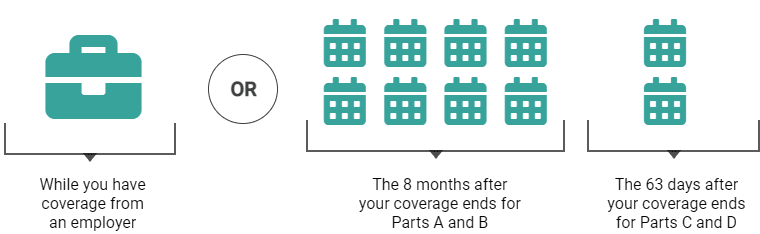

You can delay enrollment in Medicare Part A (Hospital Insurance) and/or Part B (Medical Insurance) if you’re actively employed at a company with more than 20 employees on your 65th birthday. You must also be enrolled in active creditable health care coverage through your employer, union, or spouse’s employer (see COBRA paragraph).

Once your creditable health care coverage ends—or when employment ends (whichever comes first)—you qualify for an eight-month Special Enrollment Period. It's a good idea to enroll in Medicare before you lose your employer-sponsored health care plan; this will help you avoid any gaps in your coverage. If you do not enroll in Part A and/or Part B before the eight-month window is over, you may have to pay penalties Learn more about penalties.

COBRA and retiree health plans aren't considered coverage based on current employment—so you're not eligible for a Special Enrollment Period when that coverage ends. This Special Enrollment Period also doesn't apply to people who qualify for Medicare based on having End-Stage Renal Disease (ESRD).

In 2023, Medicare established new two-month Special Enrollment Periods for Part B and premium Part A for people who experience an exceptional circumstance. This may include living in an area impacted by disaster/emergency, losing Medicaid coverage, or being released from incarceration.

If you sign up for Part A and/or Part B because of an exceptional situation, you’ll have two months to join a Medicare Advantage plan (with or without drug coverage) or a standalone Part D plan.

When is my Special Enrollment Period?

Special Enrollment Periods for Parts C and D

There are certain situations where you may be eligible to enroll in Medicare Advantage and Part D under a Special Enrollment Period (SEP). For example, you may have delayed enrollment because you had credible health coverage through your employer, union, or spouse's employer on your 65th birthday.

The Special Enrollment Period to sign up for Medicare Advantage (must also be enrolled in Parts A and B) occurs:

- During the 63-day window after your employer or union group health plan coverage ends, or when your employment ends (whichever comes first)

The Special Enrollment Period to sign up for Part D (must also enroll in Part A and/or B) occurs:

- During the 63-day window after your employer/union or Veteran’s Administration coverage ends, or when your employment ends (whichever comes first)

If you delay enrollment in Medicare Advantage (with Part D) or a standalone Part D plan past the SEP window, you may be subject to the Part D late enrollment penalty. This penalty lasts for as long as you have Part D coverage.

Other life events can trigger Special Enrollment Periods for people who already have Medicare Advantage and Part D plans. For example, you may qualify for a two-month Special Enrollment Period if:

- You move outside area current plan serves.

- You enter or leave a nursing home facility.

- Your plan stops servicing your local area.

- You receive financial assistance with Medicare through Part D Extra Help, Medicaid, or the Medicare Savings Programs (MSPs).

- You’re enrolled in or dropped from a State Pharmacy Assistance Program.

- Your plan is sanctioned or terminated by Medicare.

What is the Special Enrollment Period for Medicare Advantage plans?

If you enroll in a Medicare Advantage plan when you are first eligible for Medicare Part A at age 65, you get a “trial period” (up to 12 months) to try out the plan. This trial period, in effect, is an SEP that allows you to disenroll from your Medicare Advantage plan and go to original Medicare if you wish.

At this time, you also get a “guaranteed issue right” to purchase a Medigap supplemental plan. Under federal law, this right lasts for 63 days after disenrollment from your Medicare Advantage plan. (You also get a Special Enrollment Period to join a Part D plan.)

Questions about Medicare Special Enrollment Periods?

Contact Medicare directly by calling 1-800-MEDICARE or 1-800-633-4227 (TTY users call 1-877-486-2048). You can also get unbiased Medicare guidance by contacting your local State Health Insurance Assistance Program (SHIP). Find your nearest SHIP office using the SHIP locator button on their website.