Money-Saving Tips for Family Caregivers

8 min read

Related Topics

It takes more than love and commitment to care for an aging parent or family member. Any family caregiver can tell you that it also takes money. At first, you might not notice the incidental costs of the gasoline that gets you to and from their doctor appointments or the prescriptions you’re paying for. But as their needs intensify, so does the cost of caring for them.

An AARP study found that the average family caregiver spends over $7,200 a year to provide care. The costs are even higher for those caring for someone with dementia, approaching $9,000 per year. Where is all that money going?

Common expenses incurred by family caregivers include:

- Housing (rent, mortgage, assisted living, home modifications)

- Food

- Clothing

- Transportation

- Healthcare

- Therapists

- Respite care

- Medical supplies and equipment

If your caregiving responsibilities are starting to tap your savings account, here’s good news: there are a lot of ways to save money while you take care of an older adult. And since time is money (especially for family caregivers), let’s dive right into them.

Ways family caregivers can save money

Prescription Savings

Half of Americans over age 65 take at least four prescriptions daily. Depending on the drugs and the copay for each one, these costs can add up fast. Most people know to opt for a generic version of a prescription whenever possible. But even some generics are pricey.

What you may not know is that different pharmacies charge different copay amounts for the same medication. If the person you care for is on Medicare, review their plan to check the prices at their preferred pharmacy first. Then compare them to prices at discount pharmacies like Costco, Walmart, and Amazon.

Some of the biggest savings can be found by using apps that offer discount pricing on prescriptions. Check out GoodRx, Single Care, and Cost Plus Drugs to see if they offer lower prices or coupons for the prescriptions your family uses.

Caregiving Supplies

Incontinence products, bed pads, wound care, gloves—these caregiving staples also take a bite out of the budget every month. Keeping an eye out for sales and coupons is one way to save money on these supplies. But who has the time?

Since you know you’ll be needing them every month, consider setting up an auto-ship account with an online retailer. Since they buy in bulk, they often pass the savings on to you. And many offer additional savings when you set up an auto-ship account. This will also save you the time of shopping for them in a store. And you’re less likely to run out. Check out the savings at carewell.com, a great source for affordable caregiving supplies.

Durable Medical Equipment (DME)

This is equipment that’s used more than once, and often for several years. Think wheelchairs, walkers, commodes, shower chairs. Medicare covers a portion of the costs when you buy or rent these from a supplier that “takes assignment” from Medicare. And you’ll need your doctor to prescribe some of them if you want Medicare to cover their portion of the cost.

But there are other, less expensive ways to get your hands on some of these items. Purchase them used at a thrift store. Search your local FreeCycle or Buy Nothing groups on social media. Some non-profit organizations, like this one in Connecticut, offer a DME lending library, where you can borrow a piece of equipment for free and return it when it’s no longer needed.

Doctor Visits

Many physicians offer a choice for in-person or virtual visits for certain appointments. Opt for virtual visits whenever possible to save yourself the cost of gasoline and parking fees. If the person you care for has a Medicare Advantage (MA) plan, try to stick with healthcare providers who are in their MA plan’s network to make the most of their health insurance coverage.

Utilities

The Low Income Home Energy Assistance Program (LIHEAP) can help people with limited income pay their energy bills. To qualify for LIHEAP, your income must be under the established limit for your household size. If you’re currently receiving benefits from other government programs including the Supplemental Nutrition Assistance Program (SNAP), Temporary Assistance to Needy Families (TANF), or Supplemental Security Income (SSI), you may be eligible for LIHEAP automatically.

For information on where and how to apply, contact the National Energy Assistance Referral program at 1-866-674-6327 or energyassistance@ncat.org.

Taxes

Most of the tax breaks for family caregivers require you to be able to claim the person you’re caring for as a dependent. This means they’re a relative who lives with you, they have a gross income of less than $4,700 and they receive more than half of their financial support from you. If you’re lucky enough to have siblings who contribute to the support of a family member, they may need to sign a Multiple Support Declaration to determine who can claim the parent as a dependent.

If you can claim the family member you care for as a dependent, you can probably take advantage of the following tax benefits:

- You can claim the Credit for Other Dependents tax credit of up to $500 whether your dependent loved one is on Medicaid or not.

- You can deduct unreimbursed medical expenses for your dependents if the expenses exceed 7.5% of your adjusted gross income. This includes costs like home healthcare, adult day care, and necessary home modifications.

- You may file as Head of Household if you meet certain requirements, like paying for more than half of the household expenses. This offers a higher standard deduction. For the 2023 tax year, it was $20,800.

The Child and Dependent Care Credit is an outlier. To claim this credit, the person you care for does not have to be your dependent. But they must have lived with you for at least six months and be physically or mentally unable to care for themselves. This tax credit reimburses you for money you pay for your family member’s care while you work. This could be care provided by an adult day care center or a paid in-home caregiver. In 2023, you could claim up to $3,000 in caregiving costs for one qualifying person and up to $6,000 for two or more. More details on this tax credit are available on the IRS website.

Six states also have caregiver tax credits that cover a portion of family caregivers’ out-of-pocket expenses for providing care. These states are Georgia, Missouri, Montana, New Jersey, North Dakota, and South Carolina.

Military Base Commissary and Post Exchange (PX)

If the family member you care for served in the military, you may be able to shop for supplies, groceries, and medical equipment at the nearest military base. Prices at the military commissary (grocery store) and PX (department store) can be lower than civilian grocery stores, pharmacies, and even big box stores. Contact the base to ask if you need to bring your family member with you, or if you just need to bring their military ID for shopping privileges.

Respite Care

No family caregiver can be expected to provide all the care for an aging loved one, all the time. It takes too great a toll on our physical and mental health. Luckily, there are ways you can save money on respite care for your loved one when you need a well-deserved break.

- Some state Medicaid programs pay for respite care services.

- Some Medicare Advantage plans include respite care as a supplemental benefit.

- Beginning in July 2024, folks caring for a family member who has dementia and is enrolled in Medicare will be able to access a $2,500 respite care benefit through the Medicare GUIDE program.

- Your state may offer respite care vouchers or stipends.

- You may be able to find a volunteer caregiver via the National Volunteer Caregiving Network.

Government Benefits

Many federal, state, and local programs are designed specifically to provide financial assistance to older adults who need support. Some of these benefits may sound familiar to you. Other benefits may come as a big—and welcome—surprise.

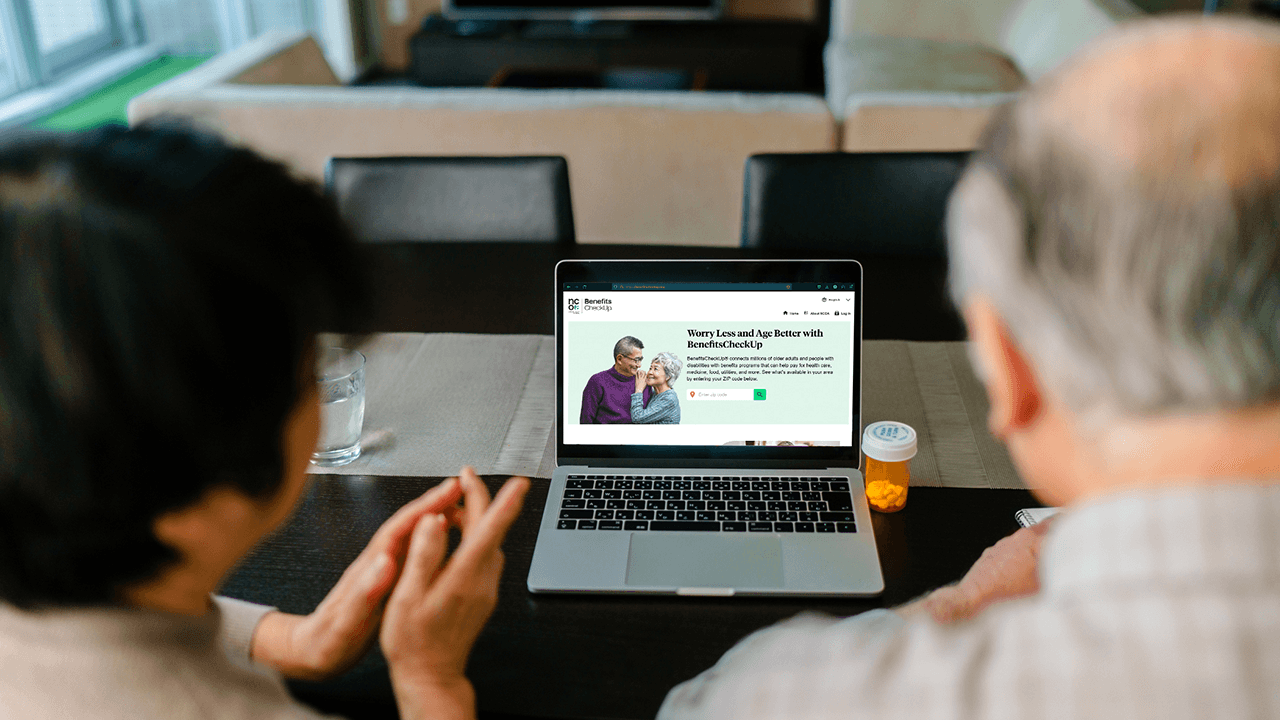

NCOA’s BenefitsCheckUp® is a free, online tool that connects millions of older adults with benefits programs that can help pay for health care, medicine, food, utilities, and more. You can explore a variety of savings opportunities for yourself, or for someone you know.

Medicaid

Each state runs its own Medicaid program, which helps cover medical costs, including long-term care, for some people with limited income and resources. Eligibility requirements and benefits vary from state to state, so check with your state's Medicaid program to see if your family member qualifies for benefits. If they don't, they would have to spend down almost all of their savings on healthcare in order to qualify. Some state Medicaid programs even pay family caregivers to provide care.

Department of Veterans Affairs (VA)

The VA is a federal agency that provides a wide range of benefits and services to U.S. military veterans. Through the VA, older veterans may have access to a pension, disability compensation, health care, home loans, insurance, and burial benefits. The VA has specialized programs to address the unique needs of aging veterans, such as geriatric care, extended care and long-term care services, vision rehabilitation, and family caregiver compensation.

If you’re caring for a veteran who has service-connected disabilities, and they live in your home, the VA’s Temporary Residence Adaptation grant can cover modifications like adding ramps and grab bars, widening doorways, installing accessible bathroom fixtures, and more.

Medicare Premiums

Did you know that low-income seniors may qualify for help paying some of their Medicare premiums with one of four federal programs? The Medicare Savings Programs can pay Medicare Part A and Medicare Part B premiums. In certain cases, they can also cover out-of-pocket expenses like deductibles, copayments, or coinsurance. While these are Medicare programs, you’ll need to contact your state’s Medicaid office to find out if your loved one is eligible.

Shoe Allowance

If the family member you care for has diabetes, Medicare will help pay for therapeutic shoes prescribed by their treating physician. This allowance covers 80% of the cost of one pair of custom shoes or extra depth shoes, plus two to three additional pairs of inserts, annually. For more information about this benefit, call the phone number on their insurance card.

Subsidized Housing

The Department of Housing and Urban Development (HUD) offers a subsidy for senior housing assistance. Section 202 Supportive Housing is for use exclusively by low-income adults over age 62 who make less than 50% of the Area Median Income. The properties tend to be accessible apartment complexes that provide support like cleaning, cooking, and transportation.

The application process can be lengthy. For information and help finding Section 202 homes, contact your local HUD agency.

Hopefully, you can use several of these—and other money saving strategies—that can help reduce caregiving costs. If you found this article helpful, share it with other family caregivers who need help reining in their care expenses. And check out the article, Finding Financial Assistance for Family Caregivers, which lays out where family caregivers can find existing money that you can access to help cover your caregiving costs.

Get Help Paying for Food, Medicine, and More

Millions of older adults miss out on money-saving benefits simply because they don't apply. Start today by answering a few questions to see if you qualify, and learn how to get help to apply